Kazakh National Bank makes inflation forecast for 2017-2018

Based on the forecasts and estimates, the National Bank of the Republic of Kazakhstan takes decisions on the monetary policy including the base rate level.

On June 3, the National Bank completed the next forecast round "April-May 2017". The forecast period is from Q2 2017 to Q4 2018.

The oil price of $50 a barrel is considered as a baseline scenario throughout the forecast period. The external inflation background and external demand estimates have not experienced considerable changes and is generally in line with the trajectories of the previous forecast round, the NB reports.

The inflation, as the main objective of the monetary policy, will continue the slowdown trend in per year terms due to stabilized inflation expectations and maintained predictability of the situation in the domestic money and foreign exchange markets. The supply shock for certain types of food, particularly vegetables and meat, observed over the last few months, is partially offset by the three-month decline of the world food price index without causing significant changes in food inflation.

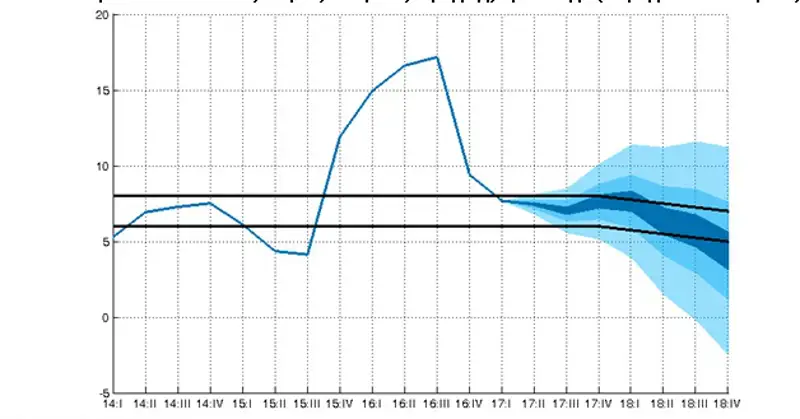

According to estimates, the expected seasonal growth of the domestic supply of food products in the summer months will contribute to a further annual inflation slowdown in the period till the end of Q3 2017. At the same time, by the end of this year the annual inflation may slightly increase because of the low base in Q4 2016. However, this effect will last for short time, and the annual inflation in 2018 will continue declining, according to the National Bank. Thus, Kazakhstan's annual inflation will be within the 6-8pct target corridor in 2017 and will start smoothly entering the target corridor of 5-7pct in 2018.

The main inflation risks are attributable to the shocks in food products supply as well as price increase by manufacturing enterprises. In case of the 40-dollar-a-barrel scenario, the risk of the annual inflation surpassing the target corridor will increase in 2017.

The pace of economic growth will speed up to 2.8pct (2.2pct according to the previous forecast round) in 2017 and to 3.6pct in 2018. The revised estimates for the growth pace come from the unexpectedly high tempos of the Kazakh economy recovery in Q1 2017. The previous forecast round expected smoother dynamics of the domestic demand growth in 2017 and acceleration in 2018. Moreover, a more buoyant pace of economic revitalization was observed at the beginning of 2017: production growth was noticed in all major sectors of the economy, fixed capital investment continued to grow; the real monetary income of the population has shown growth for the first time since November 2015. However, the domestic economic revitalization resulted in increased imports. Therefore, the higher base in 2017 affected the revision of GDP growth rates in 2018.

At the same time, the premises for economic growth in the forecast period have not changed. They presume the growth of domestic consumption against growing real wages, investment in fixed assets, production and refinery of mineral resources. Resulting from the expanded domestic demand, the growth of imported consumer and investment commodities will serve as a deterrent to GDP growth. In 2018, the real GDP will be slightly higher than its potential value, building up the inflationary pressure on the economy.

The forecast and the factual inflation in case of Brent crude oil price of $50 a barrel, in % by a quarter against the corresponding quarter of the previous year